What does AI productivity improvement mean for the VC business model? Jackie asked me about the timeline for AI adoption to start skewing how companies raise VC money, and a couple of recent posts by Brian and Connor also got me thinking about it more.

TL;DR: AI makes early product exploration cheaper and faster. That does not eliminate venture capital, but it changes where it adds the most value.

Background for anyone outside that world: VC is a high-risk asset class built on power laws. A small number of outcomes drive fund returns. The later the stage, the more evidence you have, and the lower the financing risk.

Historically, founders raised capital early because product discovery was expensive. Teams needed money to build, test, and iterate before they had proof.

AI reduces that cost for certain software categories. A small team can now run more experiments per month than before. The result is not certainty, but faster signal.

How will AI affect the VC business model?

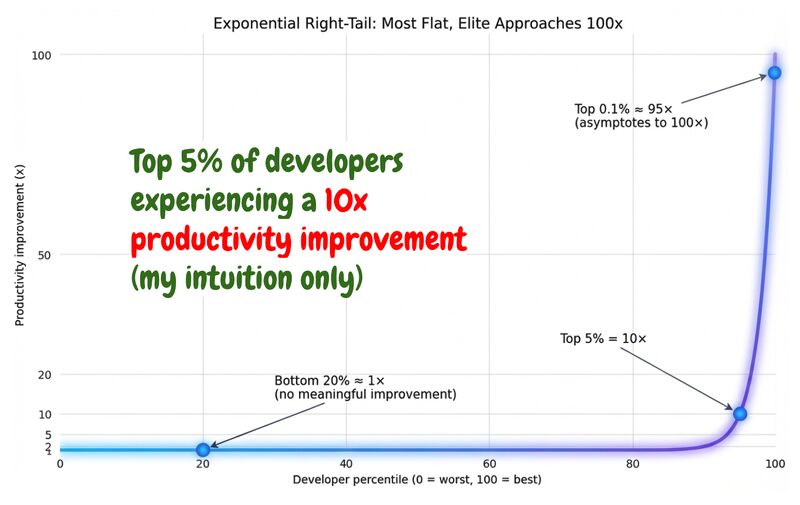

My intuition is that top operators are already seeing meaningful leverage in the build/learn loop. In many contexts that looks like a 3-10x speed/cost improvement in early execution.

That should push some financing activity later:

- more bootstrapped experimentation before the first round

- more companies reaching initial revenue before raising

- investors paying more for real evidence and less for slide decks

VC still matters. Distribution, hiring, governance, and follow-on access to capital are still hard problems. Good investors can help materially there.

But I do expect more "VC-later" companies: teams that use AI to reach clearer product-market evidence before they take dilution.

On the other side, I can also see more "founder-light" experiments where funds incubate ideas directly with capital + compute + operators.

Seed remains relevant. Growth capital remains relevant. The middle may compress for software categories where early product risk is now cheaper to test.